I LOVE the Roth IRA for so many reasons. If you qualify to make Roth IRA contributions it should be at the top of your financial to-do list. With no age limitations, I’ve already set these accounts up for my children. There are three ways to Roth (read on).

Roth IRA Benefits:

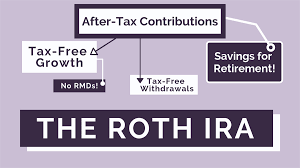

Tax-Free Growth: The main benefit of a Roth IRA is your investments grow income tax-free. However, you do need to meet a few conditions to receive the investment growth income tax-free. First, you need to have had a Roth IRA in existence for at least five years. Second, for a tax-free and penalty-free distribution of investment gains, one of the following conditions needs to be met: reach age 59.5, death, disability, or $10,000 of qualified first time home-buying expenses.

Access to Funds: While tax-free growth is fantastic, there are additional benefits of a Roth IRA. One of these benefits is the easy access you have to your own contributions to the Roth IRA. For instance, if you make two year’s of $5,000 contributions into a Roth IRA, invest it in stocks ETF’s, and the value grows to $15,000, you can still withdraw your initial investment of $10,000 at any time without paying income taxes or penalties.

This is because Roth IRA withdrawals allow you to withdraw your contributions first before having to tap into any of the investment gains.

This is a great feature that does not exist with a 401(k) or traditional IRA, because withdrawals of contributions to deductible accounts typically generate income taxes owed and a penalty tax of 10 percent if the withdrawal takes place before age 59.5. This Roth IRA feature gives people more access to their own money, more liquidity, and more flexibility. In fact, a Roth IRA can serve as a type of emergency fund.

Lower Taxes in Retirement: Roth IRAs also offer great tax savings in retirement. Because Roth IRA withdrawals of both contributions and investment gains are income tax free when taken in retirement, they do not increase a retiree’s tax liability, tax rate, Medicare premiums, or Social Security taxes.

You must have earned income to contribute and you limited to the lessor of the contribution limit or your earned income.

The annual Roth IRA contribution limit is $6,000 in both 2020 and 2019, up from $5,500 in 2018 (people age 50 or older can add $1,000), but income limits may reduce how much you can contribute.

| Filing status | 2019 modified AGI | Maximum contribution |

|---|---|---|

| Married filing jointly or qualifying widow(er) | Less than $193,000 | $6,000 ($7,000 if 50 or older) |

| $193,000 to $202,999 | Contribution is reduced | |

| $203,000 or more | Not eligible | |

| Single, head of household or married filling separately (if you did not live with spouse during year) | Less than $122,000 | $6,000 ($7,000 if 50 or older) |

| $122,000 to $136,999 | Contribution is reduced | |

| $137,000 or more | Not eligible | |

| Married filing separately (if you lived with spouse at any time during year) | Less than $10,000 | Contribution is reduced |

| $10,000 or more | Not eligible |

Two other ways to get into ROTH:

Roth 401k is awesome option with no income limitations and can later be rolled to Roth IRA:

Why I Love my Roth 401k

Roth IRA conversion from IRA Rollover is super attractive: Roth Conversion Super Attractive Now For Many People

No RMDs: Another benefit of a Roth IRA is that the account balance is not subjected to required minimum distributions after the owner of the account reaches age 70.5.

Most other retirement accounts, like the 401(k) and traditional IRAs, are subject to required minimum distributions.

A Roth IRA means that seniors have more control over when they spend their money, and are not forced to take withdrawals. This also allows the money to remain invested and to continue to grow in a tax-free vehicle for a longer period of time.

")

")

Leave a Reply

Want to join the discussion?Feel free to contribute!