Part 2. of 2. Individual Investors

Left alone, many individual investors are horrible at timing the market.

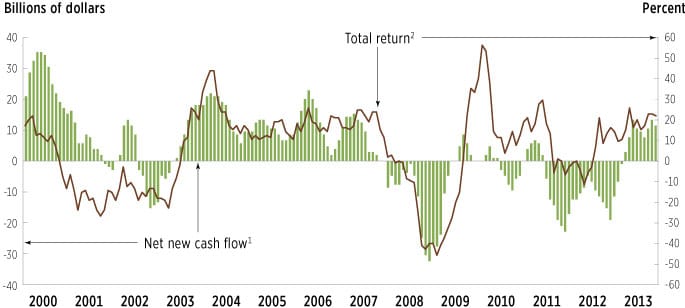

Instead of “buying low and selling high” people tend to do the opposite. The proof is in the chart below:

The terrible investor results are terrifically poor. This chart reflects the results of purchases and redemptions from stock mutual funds. Every dollar used to purchase a mutual fund is tracked and it has been found that more money tends to come in when prices are high and got out (redeemed) when prices are low. Therefore, individual investors don’t do nearly as well as they would If they just left their money to work in the investment. Are you a market timer and don’t know it? The average mutual fund equity investor holds a fund for an average of only 3.3 years. That is a short time frame for a stock fund. I’m guessing the average person bought toward the top of the market, was disappointed the returns didn’t match the recent past returns and then got out, probably moving their money into to the next hot fund.

The terrible investor results are terrifically poor. This chart reflects the results of purchases and redemptions from stock mutual funds. Every dollar used to purchase a mutual fund is tracked and it has been found that more money tends to come in when prices are high and got out (redeemed) when prices are low. Therefore, individual investors don’t do nearly as well as they would If they just left their money to work in the investment. Are you a market timer and don’t know it? The average mutual fund equity investor holds a fund for an average of only 3.3 years. That is a short time frame for a stock fund. I’m guessing the average person bought toward the top of the market, was disappointed the returns didn’t match the recent past returns and then got out, probably moving their money into to the next hot fund.

Fear and Greed create poor decision-making for investors.

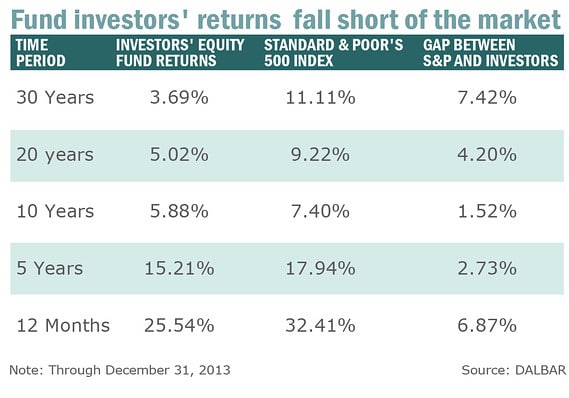

For the twenty years ending 12/31/2013 the S&P 500 Index averaged growing 9.22% per year. A very attractive historical return. The average equity fund investor earned a market return of only 5.02%. That is a HUGE difference!

I have been in this business since before “The Crash” back on Black Monday in 1987. Every major down market has had a few things in common:

- Most people never saw it coming.

- People were chasing the stock market as it was going up, thinking it would go even higher in the near term.

- When it hit the fan, and prices fell dramatically, people bailed out as fast as possible, usually near the market low.

- Now that the stock market has recovered from the last debacle in 2008 & 2009, I can say that there has NEVER been a time when the stock market didn’t recover and move past its former peak. It is true that in some cases it has taken many years for that to happen. The NASDAQ just recently reached its Dot.Com peak of 5,000. That means it took 15 years to get back to where it was.

- Investors are late to the party again in the Bull market. As you can see from the chart below there were huge redemption’s when the market was falling (selling low) and now that the stock market is back up, the net purchases finally turned positive in 2012 missing the lion’s share of the recovery.

Red line is the stock market return and green is the “net money flow”

Being an “investor” in stock (stock funds) is different from being a “speculator”. The major difference in my mind is the holding period. Anything less than five years and I consider it to be a speculative decision to own stocks (funds).

Most of us don’t own individual stocks, but we do all own our homes. Like stocks, the equity value of our homes technically could also go up and down every single day depending on what someone is willing to pay for it. Thankfully, you don’t panic and sell your home when the price goes down, and that’s in part because you don’t care about day-to-day price swings in your home value. The only time you really care is when it comes time to sell.

Ideally, you would think of your stock mutual fund purchases the same way.

When constructing a well-allocated retirement portfolio one of the key decisions is how to craft an allocation such that when the stock market drops and the headlines create more fear, the portfolio is allocated in such a way that it shouldn’t so much as to scare you out of the market. This is easier said then done.

I’ve never been smarter than any market and known when the precise time to buy or sell was going to be, but I am smart enough to know that if your portfolio allocation is aligned with your specific goal(s) than it is much easier psychologically to stay the course and ultimately be a successful investor.

Don’t wait for the next market correction.

Email me if you would like a complimentary review of the volatility risk in your current portfolio.

Related Posts:

It’s studies like this that emphasize the importance of having a level headed financial planner who has your long term goals in mind. S/he can ‘talk you off the ledge’ when the market has a sell off and convince you not to sell but rather to buy because good companies are on sale.

In addition, you want your financial advisor to not be commission based (which you typically find at banks, brokerage firms, and insurance companies) because s/he might see a market sell off as a chance to ‘move things around’ to generate commissions, whereas a fee-only advisor will look at a sell off as a chance to rebalance your portfolio to capture gains and to purchase securities at a discount instead of possibly being led to do portfolio movements simply to generate a commission check.